Build a Business That Can Run Without You

Owner dependence is the single biggest structural cap on what a company is worth, and in the AI era the same trap reappears whenever your AI leverage lives in one person's head instead of in the process.

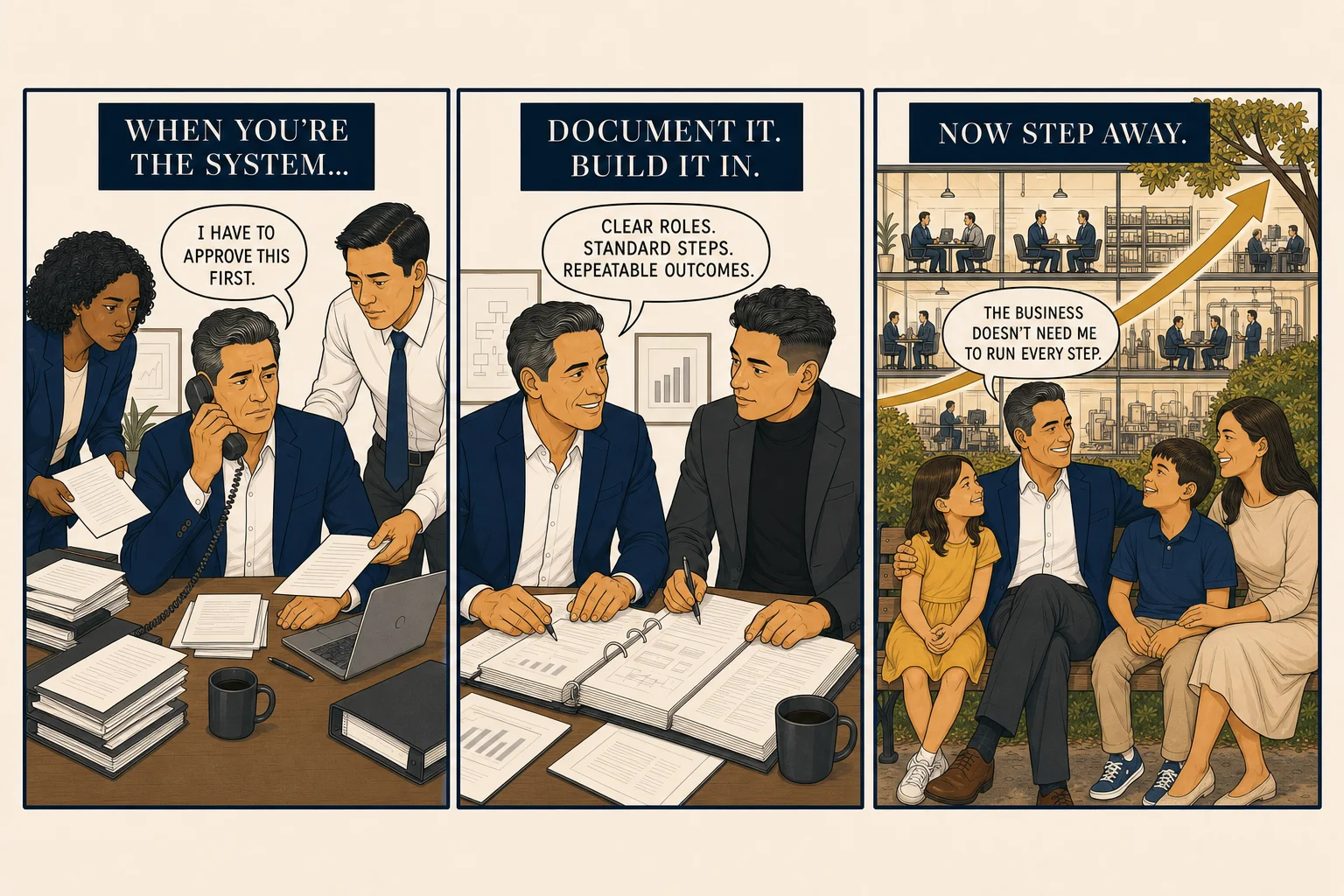

The instinct of most founders is backwards. They treat being needed as proof of value. It is the opposite. A business that cannot run without its owner is worth less, sometimes far less, than the same business with the owner extracted, because what an operation is worth is a bet on whether the cash flow survives the people who currently produce it. This page takes the strong version of that claim: owner dependence is not one weakness among many, it is the constraint that limits the others.

The Owner Is the Cap, Not the Engine

A company that stops functioning when one person leaves is closer to a job than a business. The work of operational maturity is moving from owner-operated to a state where the team and the systems run the company. Recurring revenue, a management team that makes decisions, customer relationships that do not route through your phone: each of these is really a way of saying the same thing, that the value survives your departure. Remove yourself first and the rest of the checklist becomes achievable. Leave yourself in and the others cannot fully count.

AI Has a New Version of the Same Trap

Here is the part most owners miss. AI does not automatically fix owner dependence. It can quietly recreate it.

When the AI leverage in your company lives only in the founder's head, or in one clever person's private workflow, or in prompts that exist nowhere but one laptop, you have not built a durable advantage. You have built a new single point of failure that walks out the door the same way the founder does. Leverage that one person can carry away is fragile by definition.

The fix is the same fix that always worked, applied to AI. The knowledge has to live in the process, not the person: documented, checked in, and reproducible, so the next person, and your own tools, can run it without the original author present. This is why owning the substrate and a checked-in Organizational Truth Repo matter. They are how AI leverage becomes part of the company rather than a private skill.

Documentation Is the Lever

The closest practical lever is documentation. Written-down process is how the knowledge in someone's head becomes an asset the company owns rather than rents from an individual. Standard operating procedures, treated as a real asset, are what let a business keep running when any single person leaves, and they are equally what let your AI act on how the company actually works. This is the argument in Documentation Equals Transferability and SOPs as an Asset.

The throughline is simple: build for your own absence, and build for the absence of every individual whose head currently holds something load-bearing, including the person who set up your AI. A company engineered to run without any single hero is the one that is both resilient today and worth more whenever you choose to step back.